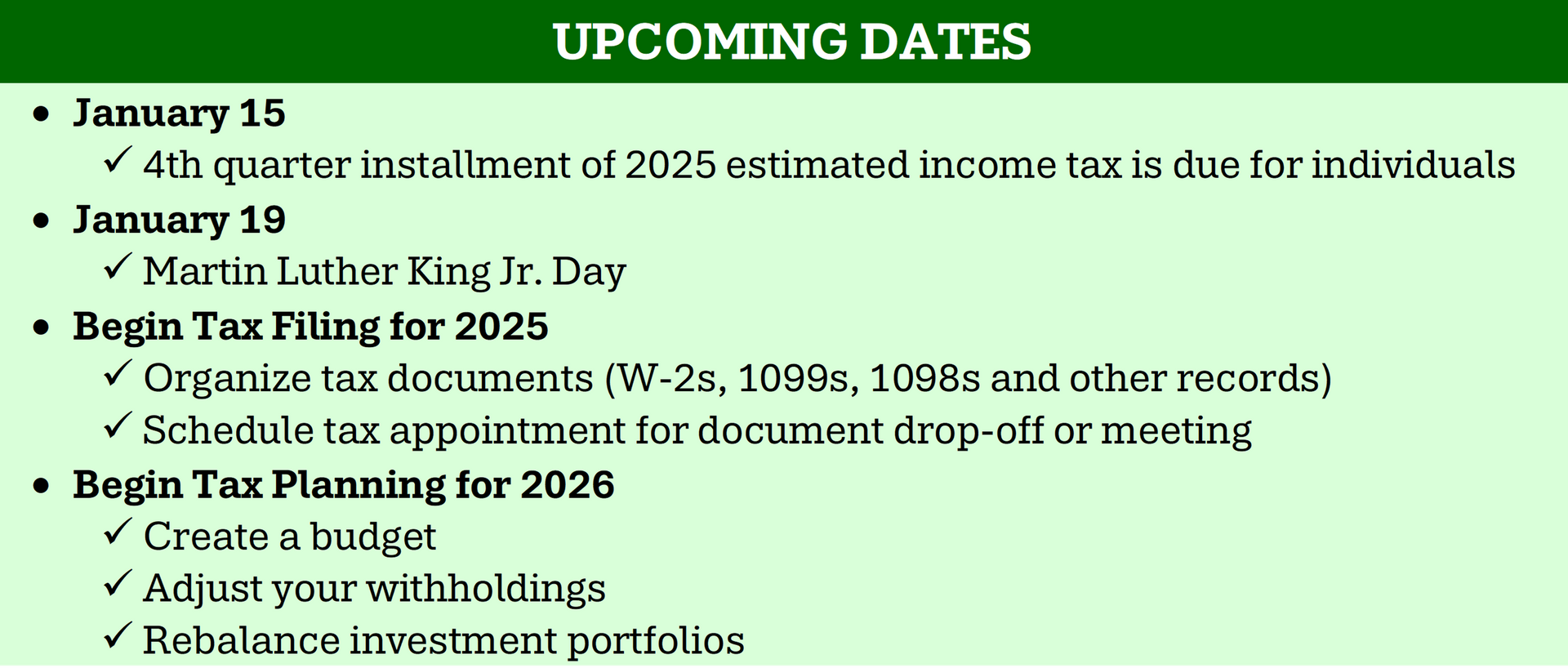

In this article, you can learn the most impactful tax-planning strategies and when it's best to file with a local CPA for an advantage over a reactive approach.

With so much uncertainty in the economy, the tendency is to step back and wait until things settle down. On the other hand the early bird catches the worm. Now is a great time to be thinking about steps to reduce your tax obligations, both this year and into the future. This month an article is presented for your review to get the ball rolling. There is also an article outlining the specifics of student loan payments being restarted after the Justice Department overruled several loan forgiveness initiatives. Rounding out this months news, and on the heals of recent lawsuit wins regarding the addictive nature of social media, is an article about the comeback of traditional, slower-paced hobbies. Want to bake some bread, anyone?

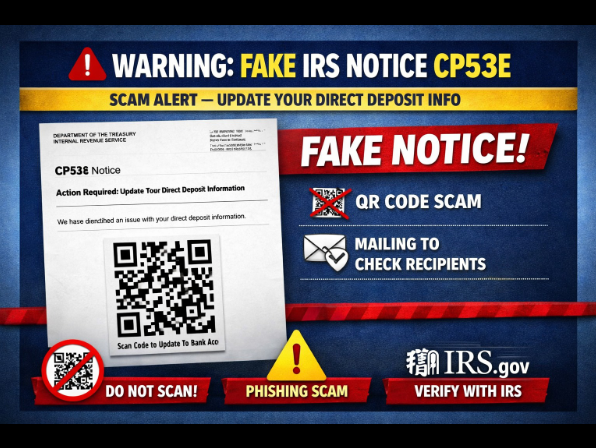

🚨 ALERT: New 2026 IRS Letter Scam (CP53E) If you received an IRS Notice CP53E about a "direct deposit change" or "unable to process refund" notice, DO NOT act immediately. Scammers are creating fake versions of this letter right now to steal your refund and personal information! 🛑 What you need to know: ✅ It’s a real letter, but often a scam: Many people are receiving fraudulent letters, while others are caught in an IRS glitch affecting 800,000+ taxpayers. ⚠️ The Red Flag: Scammers ask to click a link, scan a QR code, or provide Social Security Numbers via phone. 🛡️ Protect Yourself: The IRS will NOT send QR codes or demand urgent action via email. What to do if you receive one: Do not call the number on the letter. Do log into your secure IRS online account to verify its legitimacy. Contact us immediately to verify your tax refund status before you click anything. Stay safe this tax season!